In 2020, the clothing sector was hit hard by the economic and health crisis. World trade flows in outer clothing fell by almost 15% in euros last year, compared with a fall of more than 15% for linen and hosiery. The slump in the second quarter of the year was dramatic, reaching almost 50% for some linen and hosiery products. Furthermore, pre-pandemic levels were not recovered at the end of the year, with a decrease in the fourth quarter of 2020 of 9% for underwear and 10% for the outside world, on a trend basis.

Less intense was the collapse in world demand for home textiles, which decreased on average in 2020 by “only” 7%, but above all was found to be in clear trend growth at the end of 2020. The fall in world demand for downstream products was reflected in an even stronger fall in upstream sectors. Global demand for yarns and weft fabrics has fallen by an average of about 2020 …

The health crisis that began last year has had important repercussions on the dynamics of international trade. All the main sectors that use textile machinery have been hit hard: since the first quarter of 2020, there have been falling on a trend basis for world trade in the textile and clothing sector, ranging from -5% to -10% depending on the sector. Above all, there was a deep collapse in the second quarter, when world demand for outer clothing and home textiles fell by more than 20 percentage points; linen, on the other hand, reached -35%, as well as yarns and fabrics.

In the following quarters, we can see a gradual recovery, although at the end of 2020 pre-pandemic levels have not yet been recovered; the only exception is home textiles, which showed particular resilience, with trend changes in global demand close to zero in the last two quarters of 2020.

The case of textile machinery

Having provided an initial overview of the textile and clothing sector, in terms of production players and trade in the last year, it is particularly interesting to deepen the link between the worldwide demand for textile machinery and that of the sectors just analyzed, or those (directly or indirectly) users of such machines.

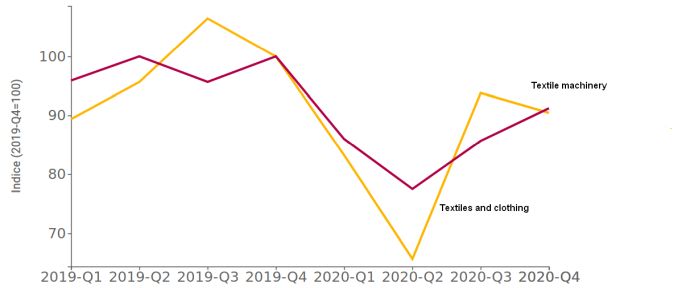

The graph below allows to analyze the dynamics of the last 2 years for the worldwide demand for textile machinery and textile-clothing products; the series is indexed, putting the fourth quarter of 2019 at 100 (last quarter not to have suffered from the serious consequences of Covid-19).

As shown in Fig. 1, the dynamics of the two curves are quite similar in the time frame considered. In 2019 there is a fluctuating trend, while 2020 opens with a sharp collapse already from the first quarter, which reaches its negative peak in the second quarter. Textile machinery, however, has limited the fall compared to the more downstream sectors.

Conclusions

The partial maintenance of investment in textile machinery does not, therefore, appear to be due to the need to expand production capacity worldwide but more likely reflects the growing competition within the sector. In order to take advantage of a competitive advantage over competing companies and face the next global economic recovery, it will be increasingly important for textile and clothing companies to be able to take advantage of the technological increases incorporated in capital goods, to support their product innovation or cost reduction processes, depending on their competitive positioning.